By understanding what a medical insurance deductible is, you can learn how to minimize your health care expenses. What is a deductible and how can it impact the cost of your healthcare? A deductible is the quantity you pay of pocket for medical services before your health insurance coverage strategy begins to cover its share of the costs.

Deductibles are a staple in many health insurance strategies, and just how much you pay toward your deductible differs by strategy. According to Investopedia, "If you get into a mishap and your medical expenditures are $2,000 and your deductible is $300, then you would need to pay the $300 out of pocket initially prior to the insurance provider paid the staying $1,700.

In addition to deductibles, there are other out-of-pocket expenditures you might be accountable for paying when you get health insurance coverage. Out-of-pocket costs include deductibles, coinsurance, and copays." is a method for you to share your healthcare costs with your insurance provider. Your coinsurance can be anything from 50/50 to 80/20 depending upon the kind of insurance plan you choose.

This suggests that a $500 procedure will only cost you $250 and the other $250 will be paid by your insurance company (how much is car insurance a month). When it comes to an 80/20 coinsurance, that exact same $500 treatment will just cost you $100, and your insurance coverage company will pay the other $400. A, or, is a flat charge that you pay for specific health care services when you have fulfilled your deductible.

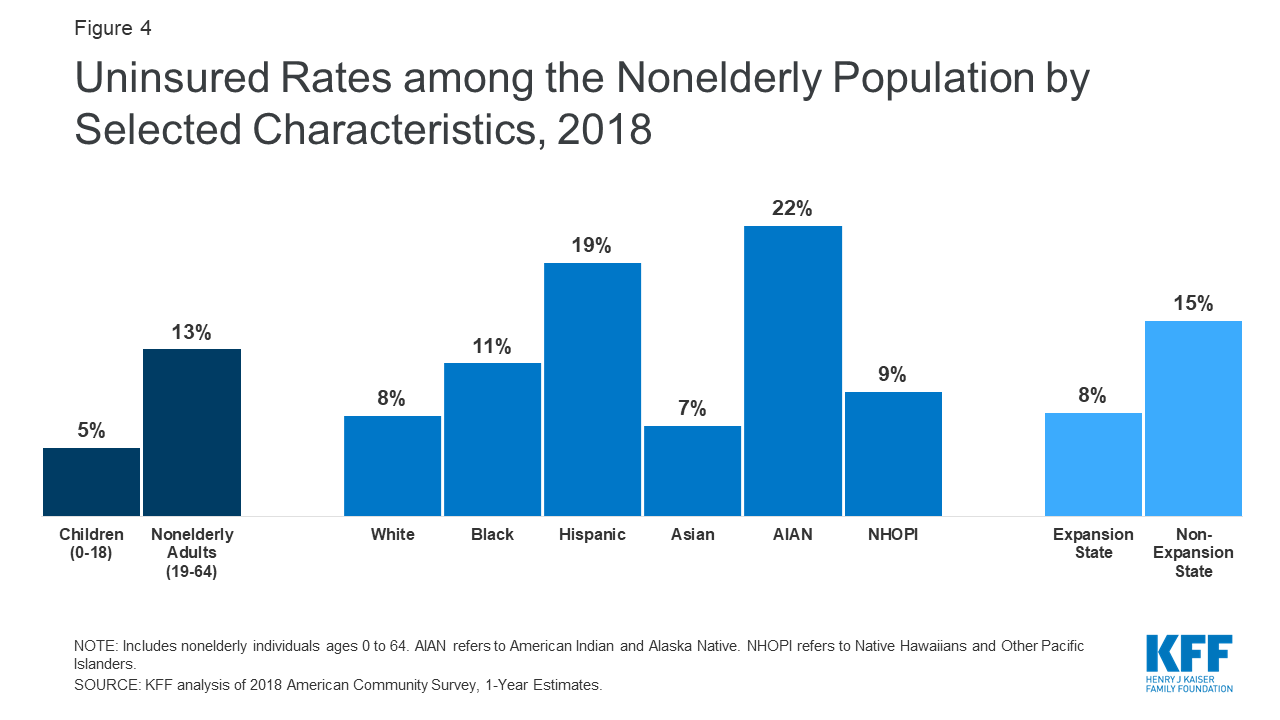

All About How Many People Don't Have Health Insurance

A copayment is a fixed expense for specific health care services that is needed at the time you get care. While most medical insurance plans include a deductible, how high or low your deductible is can vary. Normally, there are 2 types of plans:, or; and, or.

For you, the benefit is available in lower monthly premiums. If you have a high-deductible plan, you are qualified for a (). These accounts enable you to reserve a limited amount of pre-tax dollars for medical costs. When it comes to employer-sponsored health insurance, companies may contribute to their workers' HSAs, often even matching employee contributions, causing considerable pre-tax savings.

Since the money in your HSA isn't taxed like the rest of your earnings, it serves a double purpose: assisting you set aside cash to cover healthcare expenses and reducing your tax concern." Because HDHPs' monthly premiums are typically low, it can be budget friendly to individuals who are generally healthy and do not need to visit a doctor other than for yearly examinations or preventive care.

These preventive services consist of: Abdominal aortic aneurysm screeningAlcohol abuse screening and counselingAspirin useBlood pressure screeningCholesterol screeningColorectal cancer screeningDepression screening Type 2 diabetes screeningDiet counselingHIV screeningImmunization vaccinesObesity screening and counselingSexually Sent Infection (STI) avoidance counselingTobacco use screening and cessation interventionsSyphilis screeningOn the other hand, a can be helpful for people and households who require to regularly or routinely visit doctors, experts, and healthcare facilities for care.

Facts About How Do Health Insurance Deductibles Work Revealed

However you'll pay a much higher premium for these plans. Though specifics differ by place and strategy information, a low-deductible plan can cost a minimum of two times as much monthly as a high-deductible plan." Simply put, if you're seeking to keep your regular monthly premiums low, you may opt for an HDHP.

No matter which kind of plan you have an interest in, HealthMarkets can help you find the right one for your family. how much does long term care insurance cost. Contact us today to discuss http://gregoryocft990.tearosediner.net/some-ideas-on-how-to-apply-for-health-insurance-you-should-know your distinct health needs and compare your alternatives. No matter how high or low your health policy's deductible is, having the alternative to lower just how much you pay out of pocket can assist any household's spending plan.

The Premium Tax Credit is an aid that helps households making a modest earnings pay for the cost of their regular monthly premiums. You can receive this subsidy in one of two ways: You can have this credit paid to your insurance coverage business from the federal government to help lower or cover the expense of your regular monthly premiums; orYou can declare the entire quantity of credit you're eligible for in your annual tax return.

You should not be eligible for Medicaid, Medicare, CHIP, or TRICARE.You can not have access to affordable protection through your company's strategy. You must not be declared as a reliant by another person. The Cost-Sharing Reduction is an extra aid that assists households making a modest earnings manage out-of-pocket costs when getting health care.

The Ultimate Guide To How Much Is Adderall Without Insurance

In order to be qualified for this decrease, you should meet these requirements: You should have a combined yearly home income in between one hundred percent and 250 percent of the Federal Poverty Line. You should be registered in a Silver-tiered health strategy. Wish to see if you're received a health insurance subsidy! .?. !? Seek advice from a certified HealthMarkets agent today to see if your family satisfies the requirements for reduced month-to-month premiums or out-of-pocket expenses.

Make certain you can pay for to pay the premiums for the insurance plan you choose, along with cover the deductible and any copayments or coinsurance that may be required. Inspect to see what medical services use to the deductible. There are likely some medical services that the insurance plan will help cover, even if you have not yet met your deductible.

Let a licensed agent help you comprehend. When you're ready to find out more about what a deductible is, and get the protection your household requires, contact HealthMarkets. With our Best Cost Warranty, we're positive we can find affordable healthcare options with medical insurance suppliers regional to youand finest of all, we'll do it for totally free.

Contact us online to get a totally free quote, fulfill with one of our certified representatives personally, or call us at. Let's get you registered in an inexpensive health insurance today. Referrals:" Definition of 'Deductible' Investopedia." "Meaning of 'Coinsurance' Investopedia." "Meaning of 'Copay' Investopedia." "Should I Pick A High Or Low Deductible Health Insurance Plan? Forbes." 2014.

How What Is The Minimum Insurance Requirement In California? can Save You Time, Stress, and Money.

" Concerns and Answers on the Premium Tax Credit Internal Revenue Service." 2015. "In Addition To Premium Credits, Health Law Uses Some Consumers Help Paying Deductibles And Co-Pays Kaiser Health News." 2013. "Explaining Healthcare Reform: Questions About Health Insurance Subsidies KFF." 2014.

This weekly Q&A addresses questions from real clients about health care costs. Have a question you want to see answered? Submit it to AskChristina@nerdwallet. com. I am going shopping the federal Market for a brand-new health insurance coverage strategy. Though I comprehend the basics of health insurance, deductibles have me confused. I am the sole income producer, living in Houston with an other half and two children.

Given these circumstances, should I select a high-deductible plan to save cash on regular monthly premiums or a low-deductible plan with greater premiums? Deductibles are a common source of confusion, and with the huge variety of options in the Market, your difficulty picking the ideal plan is reasonable. Understanding how high- and low-deductible strategies work, how month-to-month premiums play into your decision and how these plans can impact your protection will help ensure your household has the most suitable health care strategy in the coming year.